In the years ahead, the banking sector is waiting for a growing fintech impact on the banking industry. “Uberization” may reduce the number of staff in the industry to 50%. Profitability in some areas of banking services will fall to more than 60%.

It was stated by the former head of one of the largest banks in the UK, Barclays Anthony Jenkins, back in 2015. He forecasted that the revolution in financial institutions would start with a new wave of high-tech startups. They would be more technological, faster, and cheaper in lending, payments, and money management compared to traditional large banks.

Fintech startup’s disruption of the banking industry is the thing world can’t ignore. This overview will help you know more about its trends and services provided.

World fintech market

The term fintech means software development or technological innovation in financial services. Companies working in this area usually aim to improve the existing financial infrastructure or create a new one. As a rule, they directly compete with banks.

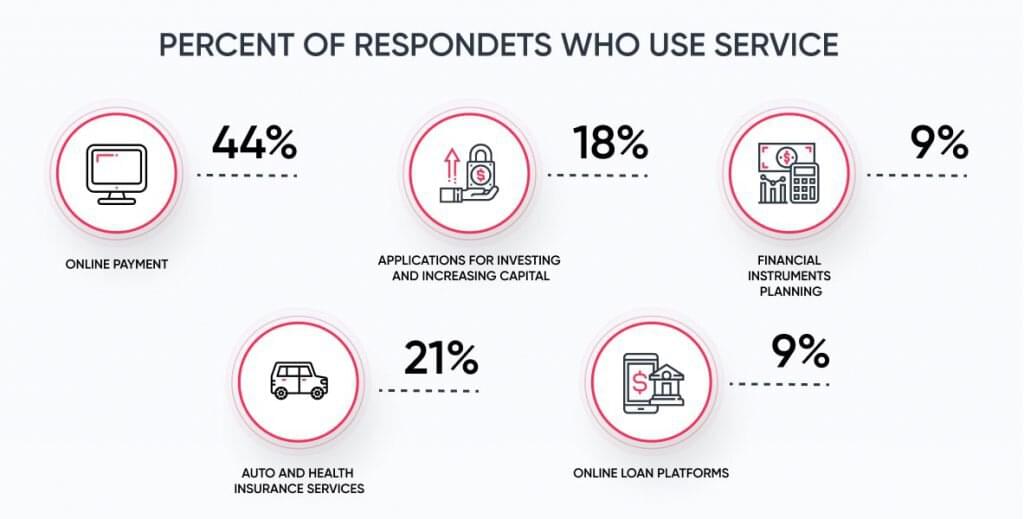

According to the Fintech Adoption Index from EY, around a third of consumers use two or more financial technologies.

According to the European Fintech report: trends, adoption, and investment, the average acceptance rate of fintech projects in the world is 33%. The United Kingdom leads with 42%, followed by Spain (37%) and Germany (35%). Switzerland (30%) and France (27%) are slightly less susceptible to fintech.

In this European market, fintech is inferior to the American in terms of investment and number of transactions. For the first quarter of 2018, 427 transactions were concluded in the United States with a total value of $ 14.2 billion, in Europe – 198 transactions for $ 26 billion, in Asia – 162 transactions for $ 16.8 billion.

Fintech services that changed the industry

The financial services market is about $ 25 trillion a year, so fintech startups are trying to “blow up” the industry to bite off some of this pie within global funding. The number of nascent fintech projects is record high – many players strive to take their place in a promising market.

Find out on how your business can benefit from distributed cloud implementation

Read more

Despite the relative youth of the industry, yesterday’s many financial startups turned into influential market players. It is an occasion to invest in fintech companies so that tomorrow they will be able to compete for projects with JP Morgan and Bank of China. Here are some examples of successful projects:

- LendingClub is a service that connects borrowers and lenders in the United States. The startup promises to lower rates by opening the loan market to many participants and increasing competition.

- Klarna is a bank providing online services. It specializes in payment solutions for online stores and credit payments. The solution is to process the payment requirements of stores and customer payments. The company acts as a “buffer,” reducing risks for buyers and sellers.

- Robinhood is a mobile stock trading application. It enables users to buy and sell stocks without any fees. The service offers exchange brokerage services for investments in public companies and US stock funds.

- Credit Karma is a service that calculates a personal credit rating and helps to improve your financial situation. The rating is free, but the application has ads for other products.

Fintech industry trends

Over the past ten years, technology has dramatically changed the way the financial sector works. The penetration of smartphones and the Internet allows creating new business models and patterns of interaction between financial institutions and customers. GR Capital has compiled a list of fintech trends, the development of which will be observed in the next few years.

Financial services on a smartphone

More when 60% of the adult population of the planet use smartphones. Making financial transactions on them is convenient and affordable from anywhere in the world. Mobile finances include transactional and non-transactional services and encompasses a few aspects — money, insurance, credit, savings, etc.

Social networks to supply financial services

Social network users report much information about themselves: a place of work, interests, a list of friends and relatives. Algorithms analyze this information to provide personalized financial services. Besides, using chatbots to make a payment or other operation without leaving the social network is convenient and easy.

Alternative payment methods

- Contactless payments. RFID technology allows consumers to pay for goods and services using their debit or credit cards. There’s no need to swipe, enter a PIN, or sign for a transaction.

- Payments using terminals. Technology allows merchants to capture required credit and debit card information and transmit it to the services provider or bank for authorization and transfer funds.

- QR codes. A contactless payment method. The transaction is performed by scanning a QR code from mobile apps. An alternative method avoids a lot of the infrastructure traditionally associated with electronic payments.

Credit marketplace and user-to-user loans

Digital platforms connect borrowers, non-bank lending institutions, and private investors. The system allows you to get credit funds to people who cannot get a loan from the bank.

Big Data and Artificial Intelligence technologies

Bots with artificial intelligence are trained and, most likely, will soon be able to service even non-standard customer requests independently. Big data and AI also help prevent fraud.

Read also: How to build a money-saving app from scratch

Read more

Digital and biometric identification

Identification and authorization of clients are some of the essential tasks for financial organizations. User identification by voice, fingerprints, and face recognition changes the idea of reliability and security during financial transactions.

Using blockchain technology

According to a PwC report, 46% of financial institutions invest in blockchain technology. Blockchain technology could be the leading platform for the industry.

What’s next?

Today, banks and financial corporations are actively investing in fintech startups. According to American Banker, 82% of US commercial banks plan to increase the volume of fintech banking investments in the next three years. In the next ten years, this trend will spread to the whole world. So fintech’s impact on the banking industry will restructure the entire business process and global financial market.

Rate this article

22 ratings, average: 4.5 out of 5