What Banking Legacy Modernization Means

Banking legacy modernization cannot be a one-off replacement; it is a program spanning core platforms, integrations, data, cloud, and delivery, implemented in manageable stages that ensure business continuity while enhancing future capability.

Real-world banking legacy modernization touches critical areas such as monolith-to-cloud/hybrid, services, open APIs, real-time data analytics/AI, and embedding DevOps/MLOps into delivery.

CHI Software’s legacy software modernization services span everything from cloud migration and API unbundling to DevOps adoption and AI-ready data foundations, offering phased development without impacting live banking activities.

According to the KPMG Banking Technology Survey 2025, data modernization has become the single biggest enabler of bank transformation — yet most financial institutions remain in the early stages of that journey. The EBA Work Programme 2025-2026 places ICT risk management, operational resilience, and digital innovation at the center of supervisory priorities. Viewed through this lens, banking legacy system modernization is as much a compliance and resilience program as it is a technology upgrade.

Is your core banking stack blocking your digital transformation agenda? We analyze your systems against DORA, PCI DSS 4.0 and AI readiness, identifying which legacy components pose the greatest operational and compliance risk.

Get a Free Legacy Modernization Assessment

Why Banks Need Legacy Modernization Now

The case to upgrade old banking systems has never been more compelling. Boards are now simultaneously under four converging pressures: rising costs of running legacy systems, increased regulatory demands, competition from fintechs and neobanks, and the hastening adoption of AI.

Keeping pace with accelerating legacy modernization trends is no longer optional for institutions under DORA and Instant Payments obligations — legacy inertia is a measurable financial and compliance liability, not a neutral position.

Rising Maintenance And Technical Debt Costs

A 2026 Accenture study found that banks spend nearly 40% of their IT budgets — sometimes 70-80% — maintaining legacy platforms. This leaves insufficient headroom for innovation. Technical debt adds 10–20% to every project cost, according to surveyed CIOs, and the talent capable of supporting COBOL-based cores is shrinking as experienced engineers retire.

The market is showing this pressure: the banking market’s world-leading system modernization was estimated at $13.29 billion in 2025 and $15.53 billion in 2026, with a 16.9% CAGR. Early movers obtain a cost advantage; delayers accrue increasing technical debt and a growing maintenance cost.

Growing Compliance And Operational Resilience Risks

The EU Digital Operational Resilience Act (DORA) entered into force in January 2025 and mandates that financial institutions demonstrate they are managing ICT risk, responding to incidents, overseeing third parties, and performing resilience testing on critical systems. Legacy platforms developed without modern security and integration standards are almost impossible to bring into compliance with regulations without redesign. In fact, the EBA Work Programme 2025-2026 highlights an expected increase in the intensity of supervision of ICT risk.

Separately, an EU Instant Payments Regulation will require all payments to be received in real time, from January 2025 onwards. A large number of legacy card and payment systems were not architected to operate in real time, bringing banks that are slow to modernize legacy apps into immediate regulatory focus.

Slow Product Delivery And AI Readiness Gaps

Where traditional banks have release cycles measured in months or even quarters, cloud-native neobanks can deliver new functionality to customers in days. The Financial Brand’s 2026 Retail Banking Trends report found that 62% of banks planned to roll out real-time payments in 2026; however, many are hindered by outdated systems.

The adoption of AI widens the gap even more. Banks cannot implement machine learning algorithms for detecting fraud, calculating creditworthiness, or creating a personalized customer experience without well-structured, clean, real-time data sources. Systems based on legacy batch-processing systems and isolated data warehouses simply cannot achieve this due to their architecture. The modernization of banking legacy systems is thus a prerequisite for any credible AI strategy.

Poor Customer Experience Across Digital Channels

The design of traditional banking systems predates mobile phones, open APIs, or the 24/7 banking standard and was built around batch processing. As a result, the consequences include slow onboarding, a lack of self-service, cross-channel inconsistencies, and the risk of outages. There were 158 IT outages at UK banks from January 2023 to February 2025, totaling 33 days of downtime. Satisfaction and retention drop, as customers find rivals provide instant, seamless digital service as standard.

Running legacy banking systems past DORA's January 2025 deadline poses a measurable ICT risk. However, a prioritized remediation roadmap could be in your hands within two weeks without disrupting live banking operations.

Request a DORA Compliance Gap Analysis

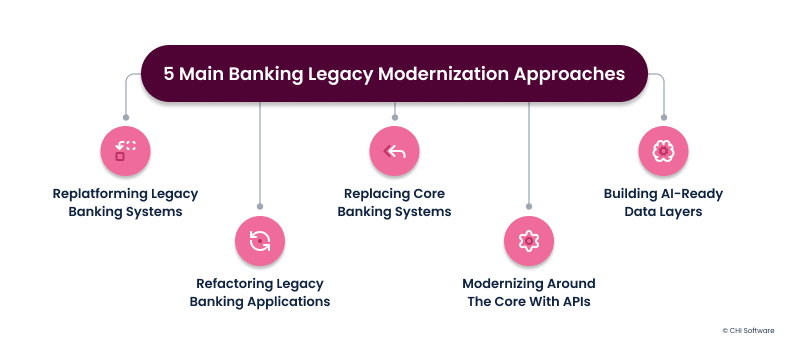

Main Banking Legacy Modernization Approaches

The right approach to banking legacy application modernization depends on each bank’s risk tolerance, regulatory position, integration complexity, and time-to-value requirements. The five principal modernization strategies each carry different trade-offs between continuity, cost, and capability.

Replatforming Legacy Banking Systems

Replatforming is the process of migrating current applications to an updated cloud or hybrid environment with minimal or no code changes. Replatforming provides increased agility, better scalability, and lower infrastructure costs without altering core business logic. For banks with stable, operational, and rigid core systems, replatforming can be the fastest path to lowering maintenance expenses and increasing availability. The bank’s operational continuity remains undisturbed while benefits of a cloud-native architecture can be realized-auto-scaling, managed services, and enhanced disaster recovery.

Refactoring Legacy Banking Applications

Refactoring restructures code, breaks monolithic systems into microservices, reduces technical debt, and enhances modularity, without affecting the outside world. The benefits include higher developer productivity, lower defect rates, and vastly simpler future integration. This should be employed in banks where business logic is locked in legacy code and where increased delivery velocity is essential. Also, the system should be designed to be open to future integrations, with an API to facilitate them. Refactoring is typically done in phases to avoid disruption of operations.

Replacing Core Banking Systems

While sidecar offers the most architectural flexibility, it also carries the highest execution risk. By 2026, IDC predicted 40% of all global banks will migrate their business to sidecars – a modern core running alongside the legacy system and taking customers out in tranches. This approach is appropriate for institutions with high transformational capacity, a clear migration logic, and executive buy-in for a multi-year change program.

Modernizing Around The Core With APIs

API-led modernization uses a modern integration layer to wrap around your old core. It allows 3rd-party access and, crucially, gives you Open Banking and opens new digital channels while still leaving the old core in place. It’s frequently the quickest route to both compliance and front-facing change. As you expose the core via APIs, your back-end systems can be updated independently behind the integration layer, transparently to your customers. Legacy banking platform modernization services (e.g., API gateway implementation and event-driven architectures) are central to this approach.

Building AI-Ready Data Layers

AI for banking requires real-time, structured, governed data. Most legacy systems are built on a batch-based, siloed architecture that can’t support modern ML pipelines. By adding a modern data layer via data lake house architecture, stream processing, and governed data contracts, AI fraud detection, real-time credit decisioning, and a personalized customer experience can be delivered. According to KPMG’s 2026 Banking and AI report, “Modernizing the data environment will be the most important enabler of Banks’ efforts to drive measurable ROI from their Generative AI investment.”

Not sure which modernization approach best fits your core banking architecture, from the payment core to the Open Banking API layer? Receive a clear technical recommendation within 4–6 weeks.

Book a Technical Architecture Review

How to Plan and Execute Banking Legacy Modernization

Good banking legacy modernization initiatives apply discipline to execution as much as to design. Reliability and business continuity are as important as clean architecture.

A structured application modernization roadmap that covers assessment, prioritization, phased migration, and governance is what separates programs that deliver on time from those that stall after the first wave.

This five-phase approach outlined below shows best practices drawn from DORA, EY Banking 2026, and the DORA 2025 year-in-review:

Assessing Legacy Systems and Dependencies

Modernization begins with a rigorous inventory. Every component must be mapped: application dependencies, data flows, integration points, infrastructure contracts, and compliance obligations. SIG’s Finance Signals 2025 report found that 37% of legacy systems carry a below-average architecture rating, more than three times the rate of modern alternatives, and these systems deliver software updates 40% more slowly. Without this baseline, migration planning remains guesswork.

Prioritizing Systems By Risk And ROI

But not every legacy system needs to be decommissioned. Ranking these by risk involves considering three drivers: regulatory exposures (DORA, PCI DSS 4.0, Instant Payments); operational risk (single points of failure, ongoing costs, talent limitations); and business value (revenue-generating, customer-impacting, supporting AI enablement). The highest-priority legacy systems to modernize are those that rank highly across all three drivers and would serve as the evidentiary basis for discussion with the board and regulators.

Planning Migration Waves And Rollbacks

The big-bang replacements present a high failure rate. A phased wave approach (migrate individual function domains sequentially) minimizes risk; each phase could be validated individually. Each wave of migration would also be accompanied by a playbook detailing the rollback and RTO. Blue/green deployment, where the new system runs in parallel until it is fully tested, has become the de facto standard for core banking migrations, as 99.9-99.95% uptime is mandated by contract or regulation.

Validating Data Integrity And Performance

Data integrity failures account for the highest proportion of delays and overspend in migrations. Data validation needs to be continuous and automated, validating record counts, transactional sums, and referential integrity between systems at each stage of the migration process – not solely at cut-over time. Performance testing at the maximum simulated load (think simulated month-end processing, highest-volume payments, and real-time API speeds) needs to be completed before go-live. For regulatory audit purposes, every data transformation must be logged, auditable, and accessible.

Managing Change Across Teams and Operations

Technology delivery is not the end goal. Cross-functional governance, including IT, operations, compliance, risk, finance, and customer channels, is vital for a successful banking legacy modernization. An organizational change and transformation office, supported by strong ownership and executive sponsorship, will mitigate some of the organization’s inherent resistance to change, which causes good programs to falter. The 2025 Year in Review of the DORA regulation found that organizations with established change practices deploy 4x more often and recover 3x faster.

Worried about downtime or data integrity during core banking migration? We start with a documented rollback playbook, an RTO of under 15 minutes and blue/green deployment, maintaining 99.9–99.95% uptime throughout.

See How We Guarantee Business Continuity

Expected Outcomes and Common Mistakes

Expected Business and Opex Benefits

With a discipline to modernizing legacy banking software, banks reap tangible benefits in four areas. Bank legacy modernization cases reveal that costs can be reduced by 38-52% in total cost of ownership, and one mid-size European bank decreased core system costs by 38% in 18 months while increasing the speed of product delivery by 62%.

The key business and opex benefits include:

- IT Cost Reduction: Eliminates runtime fees, reduces maintenance costs, and minimizes technical debt that leads to expensive emergency fixes and failed projects.

- Faster Time to Market: Uses standardized infrastructure coupled with cloud and continuous delivery to cut release cycles down from months to weeks or days.

- Scalability & Elasticity: Enables flexible capacity scaling through cloud adoption, while APIs improve system decoupling and maintainability.

- Operational Efficiency: Cleans up legacy system inefficiencies so teams can focus on shipping value rather than fighting fires.

- Data & Analytics Enablement: Improves data accessibility by migrating to modern platforms, enabling faster decision-making, real-time analytics, and fraud detection.

- Business Agility & Innovation: Transforms legacy functionality into services, increasing flexibility and accelerating the launch of new features.

- Customer Experience Improvement: Enables speed, real-time delivery, and the seamless experience modern consumers expect across multiple channels.

For a closer look at how these results were delivered in practice, see our legacy modernization examples across financial services and adjacent industries.

Common Banking Modernization Mistakes

Despite clear incentives, many programs fail or deliver significantly less than expected. The most consistent failure patterns are:

- Big-bang replacement without phased validation: Trying to cut over all of the core at one event-high risk of catastrophic failure-usually irrecoverable within the reasonable timeframes and budgets.

- Weak dependency mapping at the start: Moving forward without understanding how the integrations, data flows, and business rules are captured in legacy code.

- Poor data quality governance: Finding data inconsistencies during the migration that will delay the go-live and undermine stakeholder trust.

- Missing rollback plans: Allowing migration window entries with unproven, undocumented rollback capability, putting the bank at risk of extended outages.

- Treating compliance as an afterthought: Trying to bolt on DORA or PCI DSS, or AML requirements at the end of a migration, rather than build them in from the start.

- Underestimating organizational change: Prioritizing technical delivery over the operational, process and culture factors, which drive adoption and sustainability.

Proving Value To Boards And Regulators

For CIOs, CTOs and CFOs, the very same program tells a different story. CFOs need OPEX savings, a phased investment profile, and TCO analysis; CTOs require proof points for better architectural quality, higher velocity, and fewer incidents. CIOs and Boards require regulatory confidence through the regulatory story; DORA compliance through audit trails; and a resilience story that withstands supervisor scrutiny. Having this multi-stakeholder evidence included from the beginning into the program governance defines board-confident modernizations.

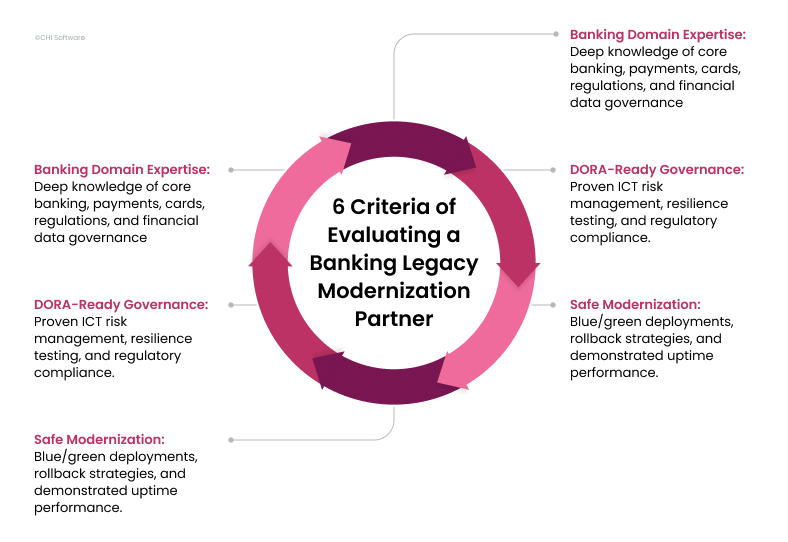

How to Choose a Banking Legacy Modernization Partner

Choosing a banking legacy app modernization partner is equally as important as deciding on your technical strategy. The wrong choice will lead to long delays, high costs, and compliance risks, while the correct choice will add depth to your banking expertise, provide a rich understanding of regulation, and a well-tested delivery approach.

Assess potential partners on these six characteristics:

- Banking domain expertise: Understanding of core banking architecture, payment systems, card systems, regulatory frameworks, and financial data governance, not just generic software delivery capability.

- DORA-ready governance: The ability to design, document, and prove your ICT risk management, incident response, and resilience testing such that it passes inspection by regulators.

- Migration safety track record: Documented blue/green deployment capabilities, tested rollback playbooks, reference engagements with concrete uptime metrics.

- Integration capability: Experience with layers of the Open Banking API, payment rails, connections to core systems, and extracting legacy data from systems such as mainframes.

- DevOps and MLOps maturity: Automation and CI/CD, together with ML deployment practices, have been embedded within the modernized delivery model, as ongoing operations, not just for migration

- ROI linkage: Translating technical achievements into tangible business results-OPEX reduction, speed to market, and compliance status-in a way that works for both board and regulatory reporting.

Ready to modernize your banking systems without disrupting operations or blowing the budget? Validate ROI and confirm DORA compliance readiness in a fixed-price pilot before committing to full-scale transformation.

Start with a Fixed-Price Banking Modernization Pilot

Banking Legacy Modernization With Predictable ROI

The argument for upgrading outdated banking systems is no longer theoretical. It’s documented, quantifiable, and increasingly imposed at the board level. Banks are now pursuing measured, staged modernizations with integrated compliance and definite ROIs in each phase, rather than the expensive, all-or-nothing transformations that often drag on for years without providing value.

CFOs now frame the argument not in terms of cost but in terms of expense. When the full costs of ownership, compliance, inefficiency, and the penalty placed on each new product delay are taken into account, the OPEX case is usually the stronger one. CTOs are aware of the future architecture, which involves cloud-native cores, event-driven integration, real-time data, and an AI-enabled infrastructure. CIOs also recognize the regulatory pressures of DORA, Instant Payments, and PCI DSS 4.0 as compelling reasons to update their systems.

Banks that act now, using a well-defined, phased plan, will achieve cumulative benefits of reduced operating costs, faster delivery, greater regulatory comfort, and AI readiness that others strive for. The only issue is not if you should, but how you do it with as little risk and as much predictable return as possible.

FAQs

-

What is banking legacy modernization?

This is an organized, phased approach to core banking, interface, data pipeline, and cloud infrastructure software development, rather than a replacement program.

-

How is it different from core banking replacement?

Core replacement is one of several modernization options. Banking legacy modernization encompasses replatforming, refactoring, API-led decoupling, and data layer transformation — many of which deliver value without replacing the core at all.

-

What is the lowest-risk modernization approach for banks?

APIs are the easiest modernization path and offer the lowest execution risk. You can retain your current core, add new digital functionality, and comply with new regulations by gradually migrating to new systems via a robust API integration layer.

-

Can banks modernize without service disruption?

Yes. It's possible to maintain 99.9-99.95% uptime when modernizing legacy banking systems by using blue/green deployments, migration waves, and rollback-defined RTO playbooks.

-

What role does AI play in banking legacy modernization?

AI readiness is the consequence and the driver of modernization. You need a real-time data infrastructure, clean data pipelines, and a cloud-native architecture in order to scale out your fraud detection, credit scoring, and personalization models.

About the author

Yana oversees relationships between departments and defines strategies to achieve company goals. She focuses on project planning, coordinating the IT project lifecycle, and leading the development process. In their role, she ensures accurate risk assessment and management, with business analysis playing a key part in proposals and contract negotiations.

Rate this article

27 ratings, average: 4.8 out of 5