It’s no surprise that banking app development is becoming a necessity today. Just think about it: the UK’s penetration rate of online banking was 98.41% in 2023, followed by Norway, Iceland, and Denmark. It’s clear that financial services have been steadily changing, and so have customers’ habits and preferences.

Financial organizations need to keep with current trends to stay competitive. But the good news is that building a mobile banking app is no longer rocket science.

We want to tell you more about digital banking app development based on our research and experience developing an instant payment app and AI-powered assistant for banking. We’ll review popular trends, features to consider, development workflow, and, of course, cost considerations.

Article highlights:

- The global mobile market is expected to grow by more than four times between 2023 and 2032;

- Digital-only banking and AI adoption are among the major mobile banking trends in 2024;

- There are at least nine app features you should consider for your mobile banking project;

- A mobile operating system (iOS, Android, or cross-platform) will have the biggest impact on your project’s tech stack;

- There are five essential steps if you want to create a banking app, and you can’t miss any of them;

- The cost of your application largely depends on your development team’s location.

Mobile Banking Industry Overview

Online and mobile banking comprise a suite of financial services offered by banks and similar credit organizations. The main feature is that the client’s account management and all transactions occur in a digital environment.

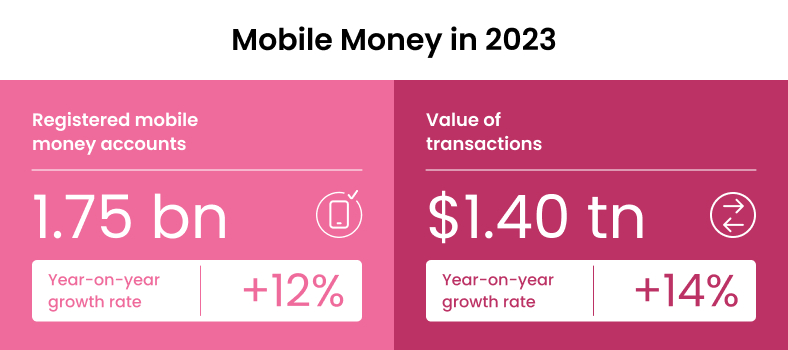

The global adoption of mobile money continues to grow.

The market for banking apps is enormous, and there are plenty of prospects for startups and aspiring new players to break into mobile banking development. Assess your prospects:

- The global adoption of mobile money (electronic wallet services) continues to grow, reaching 1.75 billion accounts in 2023, with a 12% year-to-year increase;

- The sum of mobile money transactions was USD 1.4 trillion in 2023, growing 14% over the previous year;

- The global mobile banking market is expected to reach USD 7 billion in 2032 – compared to only USD 1.5 billion in 2022;

- Android got a 67% share of the mobile banking market in 2023, although iOS users are associated with higher purchasing power, making them a target audience for premium banking services.

It’s clear that mobile payments and banking services are not going anywhere soon. Users won’t give up the convenience with which they can now access their money, leading us to the next point – trending features and technologies that can attract a wider audience.

Continue reading about RPA in banking and finance

Read more

Mobile Banking Trends Explained

Mobile banking is a multi-faceted niche providing opportunities to banks and their clients in different ways. In 2024, banking app development incorporates artificial intelligence features to improve security and other features:

- Customer support optimization through machine learning (ML) and intelligent bots. Solutions based on artificial intelligence (AI) tools like ML and natural language processing (NLP) help personalize services, predict customer behavior, and assist in making payments.

- Digital-only banking. Banks no longer need brick-and-mortar locations to provide outstanding services. Examples like Nubank, SoFi, and Chime use the full potential of existing and emerging technologies, offering speed, lower fees, enhanced security, and more personalization.

- Blockchain and cryptocurrencies. Even though this trend is not particularly new in the financial industry, the niche continues expanding year after year. Blockchain is all about security – it’s a decentralized technology that records transactions across multiple computers, ensuring transparency and immutability.

- Open Banking and application programming interface (API) integrations. Through the Open Banking system, banks allow third-party financial organizations to access customer data using APIs. On the one hand, it provides customers with additional innovative features; on the other hand, banks can guarantee the required level of security through their APIs.

- Wider implementation of voice-controlled payments. Voice-enabled access is a convenient feature that increases security against criminals. This innovation could be very effective if you supplement it with other voice services, such as conducting payments or transferring money to different accounts.

- An increase in fraud detection tools. Tracking and preventing fraud is a top priority for banks seeking to mitigate data risks. We at CHI Software use a wide range of fraud detection tools, including face recognition, strong customer authentication (SCA), and high-level standards (such as PCI DSS).

- In-app debt payments. A new trend in banking services allows borrowers to repay interest and loans in the application quickly, monitor repayment schedules, and control the state of their finances. We at CHI Software go further and implement one-touch payments, government credit line integration, and other advanced payment services.

These trends look promising! But what’s hidden behind the curtain? What important things should you consider even before consulting a development vendor? The next section will uncover some of the fundamentals.

Take this excellent moment to create your own mobile product — our consultants will explain how to build a banking app!

Contact us

What Is Worth Paying Attention To Before Building a Banking App?

Before answering “How to start a banking app?”, we need to consider some crucial points in planning and development.

Banking App Features

Before development can begin, you have to draw up clear product requirements. Here are the essential features worth mentioning:

This list of features is the foundation of any modern banking app.

- A user account with a page for registration and login. Consider a combination of security measures to activate your profile, like password login, Touch ID, or face recognition. The account must contain all information about the user: their name, bank account numbers, card details, etc.

- Key financial transactions. The application should support integration with Google Pay or Apple Pay, transferring money via systems such as RTGS or IMPS, allowing users to check balances, pay bills online, and make credit, insurance, and other payments. Many apps also offer mobile deposits and the scheduling of regular transfers.

- Transaction management. The user needs to access their entire payment history and transaction details to understand how much was debited, when, and for what. A clear transaction dashboard helps customers monitor the movement of their money and builds loyalty to your app.

- Notifications. Your app needs to inform users about each transaction and changes in their account status, warning if there are suspicions of fraudulent calls, spam, or phishing. Push notifications can also contain information about discounts, new services, bonuses, etc.

- Offline access to the account. If the application supports it, a poor internet connection (or lack of it) should not prevent the user from managing their profile. This feature can be conveniently combined with geolocation tools to allow the system to work in any situation.

- Withdrawals from ATMs without a card. Even though the world is becoming paperless, sometimes we still need cash on hand. NFC technology and QR code scanning can enable customers to access ATMs simply through their smartphones without using their cards.

If you want your app to stand out from the competition, you will need more advanced features, such as:

- Support for multiple bank accounts and cards (not all applications offer integrated budgeting – so adding this feature can help your app stand out);

- Additional financial services: for example, the Ally app allows users to earn interest on current accounts, and Truist Bank offers investment analytics;

- Wearable integration: customers will appreciate it if your app will enable smartwatches to be used for checking balances or making payments (as Bank of Melbourne does);

- AI-powered assistants. Intelligent chatbots provide 24/7 customer support and can respond to consumer inquiries instantly.

- Voice recognition. Touchless payment features allow users to ask their virtual assistants to pay their bills or complete a purchase.

Need an A-level set of features to build your own banking app? We will help with their development and implementation!

Contact us

Challenges of Mobile Banking Development

If you want to create a mobile banking app, prepare to face challenges. But there’s nothing to fear: if you are forewarned, you are forearmed, and professional engineers can help you cope with the risks.

Among the notable challenges worth mentioning in the first place are these two:

- Data, transactions, and client security;

- The need to comply with national and international legislation in finance, crime prevention, and personal data protection.

Most financial institutions cite security as their top concern. To ensure the protection of information and client money, it is necessary to:

- Think over the network architecture and choice of cloud data storage;

- Provide digital signatures and multi-factor authentication when logging in to the system;

- Enable an in-app timer for system usage sessions and strong encryption.

You can also develop an online banking application like Revolut that uses the transport layer security (TLS) protocol to authenticate clients and check data integrity.

Learn how to create an app for saving money

Read more

The system’s features and purpose determine which laws and regulations that your application must follow.

Apps that support card transactions must follow the PCI DSS security standard. If you plan to store your clients’ data, then you must comply with the European GDPR directive, California CCPA, or similar territorial regulation. Are you going to provide payment services in the EU? Take steps to comply with the PSD2 directive.

These are all rules you need to consider before starting the development process – make sure to hire a financial consultant or IT business analyst to help.

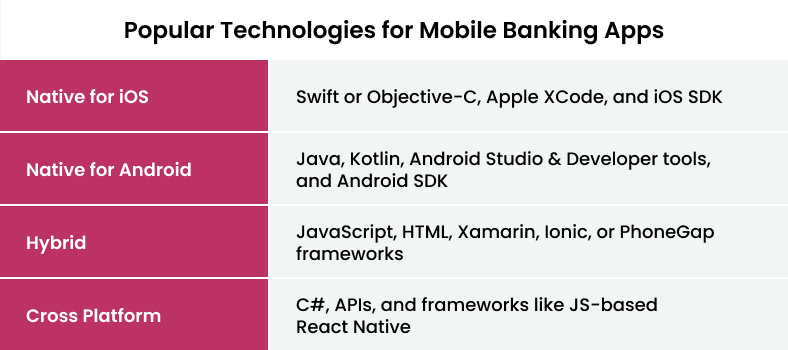

Tech Stack to Build a Mobile Banking App

What tech tools to consider if you plan to build a banking app

Understanding the required technology stack will help you better define the budget and time needed to develop a banking application. You’ll need technologies for:

- Front-end development (native, hybrid, or cross-platform);

- Creation of the server side software – concentration of business logic and the main connecting link between your mobile application and third-party processing and service providers;

- Integration of third-party services: application programming interfaces (APIs), cloud servers, payment systems, etc.

Your decision should be guided by business needs, your budget, and your desired development schedule. Native apps are reliable and high-performance, and Android and iOS features reduce reliance on third-party APIs. Hybrid applications have a single codebase and can be used across platforms.

AI and ML in fintech: use cases and business benefits

Read more

We also recommend using separate cross-platform tools to create parts of the application. For example, front-end Node.js provides many tools and libraries to build a robust framework. Flutter can be an optimal cross-platform solution that reduces future support costs and simplifies development in general by compiling a single code base for multiple platforms.

To configure the server side and ensure fast and trouble-proof work, you can use a mobile back-end as a service (MBaaS) and out-of-the-box APIs. As we know from practical experience, they reduce workload and give you flexibility in building an app.

The Most Popular APIs for Banking App Development

We’ve already briefly mentioned some of the APIs’ capabilities, but now it’s time to dwell on them more in the context of your tech stack.

Simply put, an API is a mediator between two separate programs, allowing them to exchange data. Developers don’t have to write all of the code from scratch – instead, they can use the features of third-party solutions via its API.

As you might guess, APIs can save resources on any project, providing your development team with ready-made features that are ready to be put to use. Here are the most popular APIs in mobile banking development.

- Plaid API connects applications to bank accounts, enabling user verification, access to transaction history, and balance checks.

- Yodlee API also offers account verification, as well as transaction data and financial analytics. Yodlee is beneficial if you want to provide some personalization through budgeting, expense tracking, and financial planning.

- Visa Direct API facilitates real-time person-to-person (P2P) payments and business payouts on any level, from local to global.

- Stripe API is hugely popular for managing online payments and transactions on e-commerce and service platforms. Stripe supports payment processing, subscriptions, and billing.

- Twilio API allows developers to set up in-app notifications, two-factor authentication, and customer support. Twilio is helpful when adding voice, video, and messaging functions to your solution.

It’s time to discuss the next steps to get started developing a mobile banking app. We’ll gladly share what we’ve learned so far.

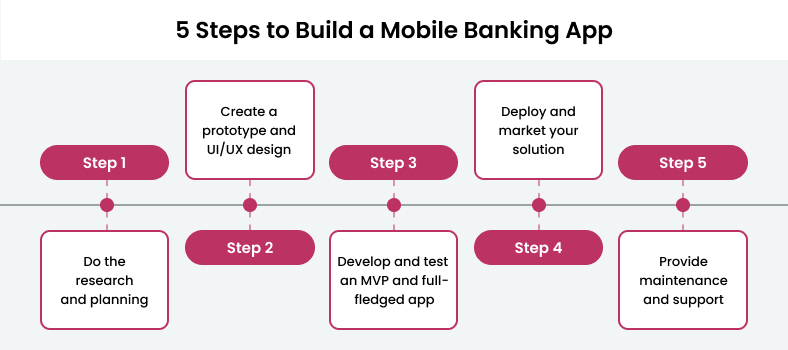

How to Make a Banking App in 5 Steps (Recommendations Included)

There are essential roadmap steps for when you build a banking app:

The essential steps for developing your own mobile banking tool from scratch

Step 1: Research and Planning

In the phase of discovery and research, you have to:

- Define your target market, core issues, and the solutions you can offer;

- Identify competitors and analyze their offerings;

- Evaluate the best procedures and make a detailed development plan.

These steps may sound too generic. Why would you spend time preparing if you can start mobile banking application development right away? Of course, you can. But then you should consider the risks, such as lack of market demand or little to no competitive advantages.

Trust us, the discovery period is essential. Good decisions now can define your future success and ensure a higher return on investments. If you need guidance, you can always come to our team of business analysts, who will help you understand all the vital questions and put together a solid plan.

Step 2: Prototyping and UI/UX Design

Every app starts with an idea, and a prototype demonstrates that idea by showing the structure and function of design elements and visuals. Designers start working first because developers need to understand the app’s navigation before coding it.

CHI Software’s designers begin with low-fidelity UI wireframes, UX design, and layouts. Our task here is to sketch a home screen, user profiles, and dashboards and then turn all of it into a high-fidelity prototype.

While creating the UI/UX design, we consider the specifics of fintech products, customers’ cultural differences (for instance, right-to-left localization for Arabic texts), as well as iOS and Android guidelines.

Among the important recommendations from our team are:

- Pay attention to visual uniqueness. Typography, icons, color palette, and elements should match your style and brand and distinguish your product from competitors.

- Make sure the navigation reflects the mobile banking app architecture. In the case of fintech solutions, it should be easy to understand, and minimize the number of steps required to complete transactions.

- Take proper care of the app’s accessibility. You may take an innovative approach, like providing voice commands, or more traditional features, like using high-contrast modes or screen reader compatibility.

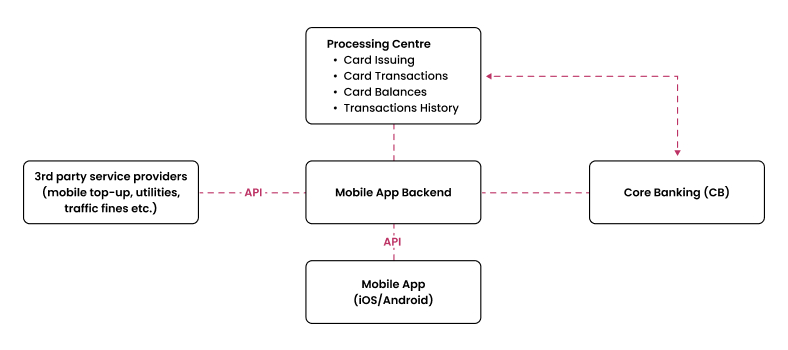

Step 3: Mobile Banking App Development and Testing

The next challenge is to bring the finished design to life with front-end and back-end development. The front-end means creating a user interface, while the back end involves configuring the server side database integration, and other functionalities.

When banking app developers create an app, they need to combine the user interface with all the functionality, and external tools, such as APIs, payment gateways, and a cloud platform.

The insides of the mobile banking app

In most cases, we recommend a safe option for starting a banking app, which is to create a minimal viable product representing the basic features and design elements of your banking app. Why only the basics? With MVPs, you can test out the liveness of your solution much faster than it could be when developing full-fledged software. And, of course, you’ll spend less money on a smaller version.

Once a product has been created, it must be thoroughly tested using a combination of manual and automated techniques. Our QA engineers check:

- Functionality and performance,

- Peak performance,

- Integrations,

- System components.

Once everything checks out, the app is prepared for release.

Important note! Our team is a big fan of the agile development methodology, and we recommend you check it out for your fintech projects. Agile principles allow you to build applications iteratively, i.e., by breaking the workflow into phases. This step-by-step process will help you incorporate feedback and make improvements continuously, avoiding major risks and errors.

Step 4: Deployment and Marketing

To send your app to the Google Play Market and the Apple AppStore (or maybe to the Microsoft Store, too), you need to prepare screenshots and all information about the application, check if the app’s performance is adequate, and ensure your solution complies with the store’s requirements. It is convenient to use the Play Market and AppStore guidelines so you don’t miss anything.

Most importantly, you should make your app attractive. Reduce complex terms into easy phrases everyone can understand. A good call would be to use keywords related to your competitor’s products.

Once your app appears in the stores, you should keep an eye on ratings and comments that come in and provide your customers with the necessary feedback. If you focus on iOS products, you can submit the app to Apple’s editorial team for an expert review.

Building a solid marketing strategy is equally important as developing an app. How would anyone know about your great solution if you don’t talk about it?

Your marketing plan should include social media, content marketing, and influencer partnerships to make your banking app a hit.

Step 5: Support and Maintenance

But the app launch is not the end of the journey. You must provide further maintenance and quick support in case of problems and consistently update features to ensure the app works with the latest OS and mobile platforms.

That’s what our team recommends focusing on this stage:

- Regular checks of security patches and documentation;

- Monitoring industry trends and competitors to make sure your app does not lag behind;

- Providing 24/7 customer support. If resources are limited for customer support staff, our advice is to use generative AI tools – a ChatGPT integration with some customization can help you tremendously!

- Keeping users engaged with personalization, financial tips, and in-app rewards. Remember to measure user engagement to analyze what you’re doing right, and what you can improve on).

The Cost of Developing a Mobile Banking App

To answer the question of how much it costs to develop a banking app, you need to know the factors with the biggest impact on the final cost:

- Application concept and definition of its functions;

- The work time of technical specialists who develop a banking app;

- The work time of designers who create the corporate identity and design of the system;

- Application integration with banking and payment systems, implementation of security measures, and other additional options;

- Scope of warranty service and support after the app’s delivery.

Here are cost variations based on the current market conditions.

The cost to build a mobile banking app in different locations

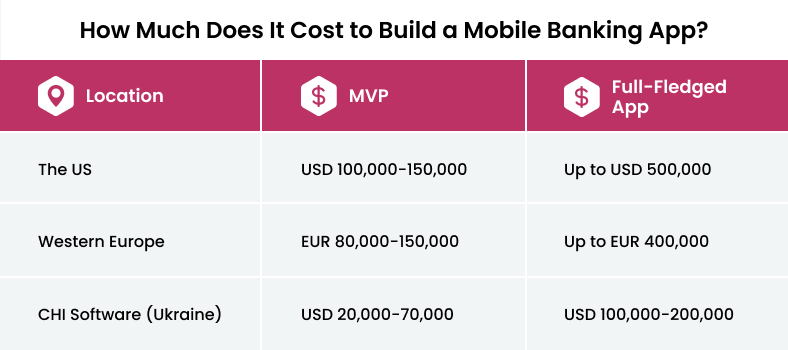

United States

Building a banking app in the US typically ranges from USD 100,000 to over USD 500,000. This higher cost is due to higher labor rates and stringent regulatory requirements. A simple app, like an MVP, may cost around USD 100,000 to USD 150,000, while a more complex app with advanced features, such as real-time market data integration and financial planning, can exceed USD 500,000.

Western Europe

In Western Europe, mobile banking application development costs are slightly lower than in the US but still substantial, ranging from EUR 80,000 to EUR 400,000. High labor costs and strict compliance requirements similar to those in the US contribute to this pricing. Developing a basic MVP app can cost between EUR 80,000 and EUR 150,000, while a complex app can go up to EUR 400,000.

CHI Software

CHI Software offers a more cost-effective mobile banking app development, ranging from USD 20,000 to USD 200,000. The lower cost of labor in Ukraine significantly reduces the overall development expenses. An MVP might cost between USD 20,000 and USD 70,000, whereas a more complex app can range from USD 100,000 to USD 200,000.

Looking for accurate cost data to build a mobile banking app? Contact us for a quick calculation of an individual estimate

Contact us

Create Your Own Banking App with CHI Software

The executing company‘s rate is the main factor influencing a mobile app’s cost. But in pursuit of a reasonable price, you cannot sacrifice the quality of the finished product. That is why companies and startups around the world choose Ukrainian development services. They are distinguished by the best balance between high-quality services and reasonable prices.

By collaborating with CHI Software, you get this balance alongside our expertise in innovative technologies and careful attitude to project data. But that’s not all.

Ready to start a mobile banking app? Make your idea a reality — now!

Contact us

Why CHI Software? Our Experience in Banking Application Development

- Our working language is English, and we successfully communicate and partner with companies all over the globe;

- We are always open to negotiation and tend to offer our customers the best price to quality ratio;

- Creating a favorable business climate is our goal when negotiating with every customer;

- CHI Software has experts with PMP, Oracle, Microsoft, MSCA, ISTQB, AWS, BEC Vantage, CPE, and CELTA certifications.

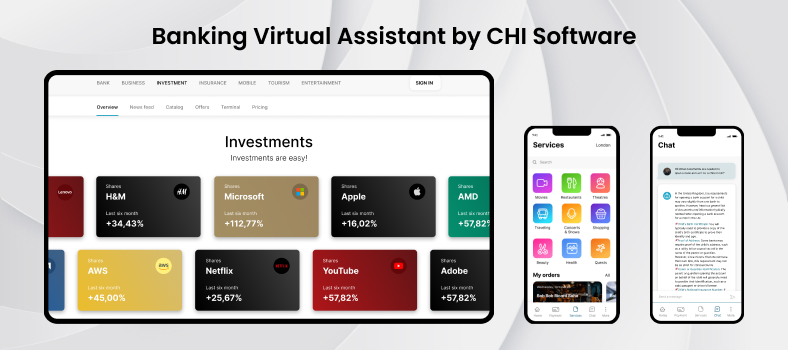

An optimized banking solution with AI chatbot integration

Let us illustrate our capabilities with an example of a finance solution for banking that we successfully developed. Our client, focused entirely on digital financial services, decided to work with us to improve a server app and its performance to attract new customers.

CHI Software’s dedicated team implemented performance testing and suggested migrating from Spray HTTP to Akka HTTP. Moving to (Twitter) Finagle HTTP client helped to reach the best results. During the process:

- The productivity of monitoring was improved thanks to OpenTracing, Zipkin, and Grafana dashboards;

- Development productivity increased through migration from Kryo to Protobuf, .proto file generation using Scala Macros – this solution made updating the app safer;

- Newsfeed aggregation was added as a secondary service to attract new customers;

- A conversational AI chatbot was implemented to answer customers’ queries 24/7.

As a result, we increased the general performance of the service. The application became safer and now works faster due to the migration to Protobuf, while AI chatbot development helped our client attract prospects and increase user engagement. Finally, in just one fiscal year, the client announced a revenue increase of 33 percent.

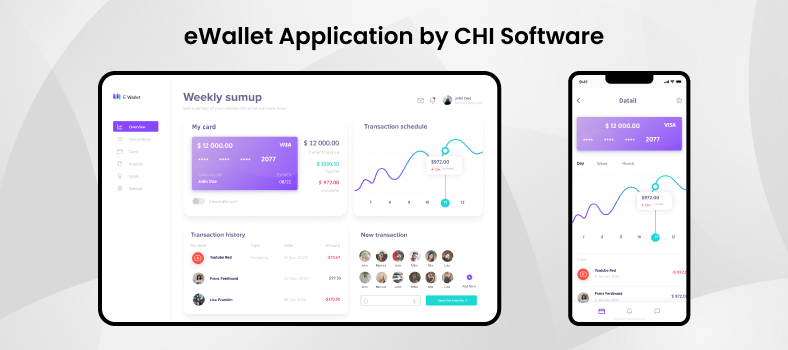

Here’s another example. One of our clients is a fintech startup focusing on innovative smart solutions for daily financial operations. Their request was to create an e-wallet app that allows users to operate money via the web, Android, and iOS smartphones using contactless payments.

This solution allows users to manage their money via the web, Android, and iOS platforms.

The project aimed to consolidate the finest fintech app practices in contactless, cashless transactions into a single online and mobile solution, improve its security, and give end customers an innovative digital experience. The CHI Software team completed all tasks within the estimated deadlines. You can learn more by reading the case study details.

Our solution’s main features include:

- Connecting different bank accounts in one place;

- Depositing money into an account;

- Secure money transactions;

- Contactless payments via near-field communication (NFC);

- Real-time analytics;

- Push notifications;

- Geolocation;

- Data synchronization.

Read our other case studies on digital payment gateways, insurance operations, and instant payments. The world of fintech is diverse, and we readily provide our clients with the latest innovations and optimization strategies.

Conclusion

Mobile application development for banking is challenging and full of subtle nuances. But do not be afraid of difficulties on the way to success. We hope this article demonstrates online banking’s potential and the latest innovations. Voice-enabled payments or digital-only banking services? That’s for you to decide.

With accurate planning, a roadmap, a realistic budget, and a strong development team, you can offer users a product that improves their financial experience and starts to bring you profit after just a few months.

The world of mobile banking development is diverse, and so is CHI Software’s expertise. Whether you need a simple MVP or a complex AI-powered solution, we’re always here to assist you. What’s next? The flow is simple: describe your app idea briefly in this form, and our sales managers will contact you within one working day.

FAQs

-

What are the key differentiators of CHI Software’s mobile banking app development services compared to other providers?

This is how CHI Software is different:

1. Experience. There are not many in the software development market with dedicated experience in developing mobile banking applications. CHI Software has seen a lot in nearly two decades, witnessed and implemented a lot of trends, and, most importantly, dealt with a great number of client needs and requirements;

2. Expertise. We offer something unique to the standard set of mobile banking features because we also have a dedicated artificial intelligence (AI) team specializing in smart chatbots, computer vision, and data science;

3. Security focus. We’re obsessed with security in all our projects, not only fintech. That’s something we’ve been taking a huge care of because of the growing number of threats. Our engineers implement advanced encryption, multi-factor authentication, and secure coding practices so you never have to worry about the app’s safety;

4. Profound customization. Each of our projects is unique, meaning we’re well aware of how to meet the individual needs of our clients. Our team uses best practices to build one-of-a-kind solutions with high-quality code and user-centric designs.

-

What is the estimated cost of building a banking app with CHI Software?

The cost of building a mobile banking app with our help is USD 20,000 to USD 200,000. The range is so broad because each client has different features in mind. If we have to build a simpler app version, it would cost you between USD 20,000 and USD 70,000. When it comes to a full-fledged solution with, for example, AI features, the cost can range from USD 100,000 to USD 200,000.

-

How long does it typically take to develop an online banking application with the CHI Software team?

The final answer depends on the scope of work. For a basic set of features including account management, transaction history, and simple fund transfers, the development usually takes three to six months. More complex functionality adds more days to this timeframe, extending to nine months or more. Feel free to contact our team for rough project estimates after the first call.

-

How do you ensure the security of a mobile banking app?

There are several key security practices that our team follows religiously:

- Encryption of all transmitted data with the help of SSL/TLS protocols;

- Providing multi-factor authentication, including biometric access with fingerprint or face ID;

- Security in the form of code reviews and regular audits;

- Performing penetration testing, which simulates attacks to test for security weaknesses;

- Complying with financial regulations, such as GDPR, PCI DSS, and PSD2.

-

How do you handle updates and maintenance for the mobile banking app?

Updates are crucial not only for the product’s competitiveness but also for its security. Here’s how we approach our work in this regard:

1. Ensuring our updates are regular in the context of new features, performance improvements, and bug fixing;

2. Immediately deploying security patches to address vulnerabilities;

3. Continuous monitoring of the app’s performance and availability;

4. Actively collecting user feedback for informed improvements and enhanced user experience.

About the author

With 5 fabulous years under his belt, Artem is an iOS developer with experience in everything from healthcare and social apps to food & booking platforms and even entertainment. He's a wizard at crafting apps that are not just easy to use but totally engaging. Whether Artem's building an app from square one or stepping in mid-project, he's a go-to expert for making digital magic happen.

Rate this article

22 ratings, average: 4.5 out of 5